More than two years into Russia’s large-scale invasion of Ukraine and European military spending is witnessing a return to levels not seen for a generation following the so-called ‘peace dividend’ won with the conclusion of the Cold War between Western powers and Soviet Russia.

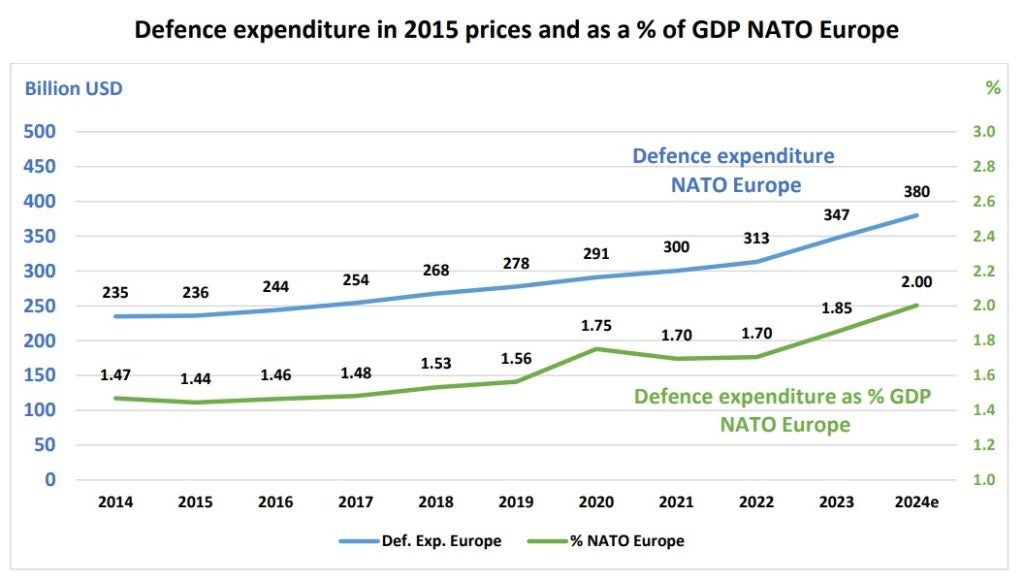

In February, Nato Secretary General Jens Stoltenberg announced that since 2014 European Nato members, along with Canada, had added more than $600bn in defence spending. In 2023 alone, Nato saw an 11% increase in defence spending in European Nato states and Canada, indicating a levelling out of burden sharing in the Alliance.

Secretary General Stoltenberg revealed an expectation that 18 Nato members would meet the 2% defence spending benchmark in 2024, representing a purported “six-fold increase since 2014”, when just three Nato states met the target.

“In 2024, NATO Allies in Europe will invest a combined total of 380 billion US dollars in defence. For the first time, this amounts to 2% of their combined GDP,” said Stoltenberg in a 14 February Nato release, adding: “We are making real progress: European allies are spending more. However, some still have a ways to go. Because we agreed at the Vilnius Summit that all allies should invest 2%, and that 2% is a minimum.”

Washington calls out Europe, again

The importance of European defence spending retains significant traction in the military heartbeat of Nato – Washington, DC. The previous Republican administration inside the White House made no secret of its dissatisfaction with European inactivity in defence spending and is a trend that remains current to the present day.

US Representative Mike Rogers (R-AL), chairman of the House Armed Services Committee, delivering remarks on 10 April 2024, at a hearing on US military posture and national security challenges in Europe, stated that “[North Korea Supreme Leader] Kim [jong-un], [China President] Xi [Xinping], and the [Iran’s] Ayatollah [Khomeini] are eagerly aiding and abetting [Russian President Vladimir] Putin’s brutal invasion of Ukraine”, and that a Russian victory would “seriously undercut” the credibility of US deterrence.

“A Russian victory will embolden Kim, Xi, and the Ayatollah to confront South Korea, Taiwan, Israel, and ultimately, the United States, in new and fatal ways. And I fear Putin will use a victory in Ukraine as a springboard to invade Eastern Europe,” Rodgers said.

To this end, Rodgers, calling for Congress to pass the long-delayed $60bn supplementary military budget intended to provide aid for Ukraine and Israel, also urged European members of Nato to spend more on defence.

“The [US] President [Joe Biden] needs to force our European allies to do more. While the UK, Poland, the Baltic states, and the Czech Republic are punching well above their weight, there are some European countries that can and must do more,” said Rodgers.

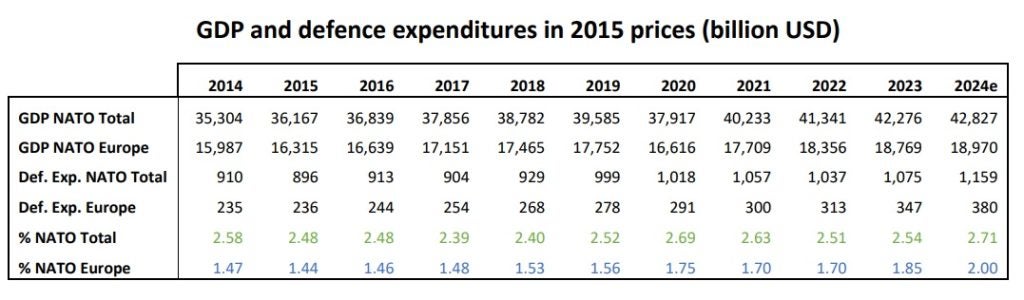

According to Nato figures, in 2014 European member states invested 1.47% of their collective GDP in defence, with that figure since rising over the following decade, reaching 2% in 2024.

European Nato members have donated significant quantities of armoured vehicles, support vehicles, artillery, and other platforms to Ukraine since Russia’s February 2022 invasion, with the UK alone contributing Challenger 2 main battle tanks and Bulldog armoured personnel carriers, along with dozens of other transport and logistics platforms, as well as long-range fires capability with the AS90 155mm self-propelled howitzers.

Germany too has been a key provider of equipment, along with France, with countries across Nato also committing in-service capabilities to Kyiv, such as Slovenia’s provision of 28 of its M-55S tanks.

In the midst of this unprecedented commitment of military materiel to Ukraine, with its war against Russia primarily being fought in the land domain, European countries also looking to replace capability gaps created as a result, while also continue long-standing modernisation efforts initiated well before Moscow’s naked ambition to reassert physical control over its near neighbours.

Europe leading global miliary vehicle procurement

Analysis carried out by GlobalData shows that the global military land vehicle market valued at $29.9bn in 2024, is projected to grow at a compound annual growth rate of 4.5% over the next decade, reaching $46.5bn by 2034 and cumulatively value $414.1bn over the forecast period.

The market itself consists of eight categories: armored personnel carrier, infantry fighting vehicle, main battle tank, armored multirole vehicle, tactical truck, support vehicle, armored engineering vehicle and light utility vehicle. The market is expected to be dominated by the infantry fighting vehicles segment with a market share of 33.3% of the total market, followed by the main battle tanks segment with a share of 27.5%.

According to GlobalData, among geographic segments, Europe is projected to dominate the sector with a share of 38.3%, followed by North America and Asia-Pacific with shares of 22.8% and 22.4% respectively.

This dominance of Europe in the land vehicle market is indicative of the requirements of the continent’s countries at present, with a Russian state engaged in a state-on-state, conventional war inside its geographical borders. In terms of geopolitical structures, Russia invaded a state in Ukraine that shares borders with both European Union and Nato member states, notably Poland.

The threat to Europe from Russia is not limited to the immediate locale of Ukraine, but also stretches north to include the small Baltic countries of Latvia, Lithuania, and Estonia, which effectively block Russia from its Baltic exclave of Kaliningrad.

However, the facts of the matter show a growing move by European countries to share more of the Nato security burden, perhaps jolted into action by a war in Ukraine that shattered the naïve preconception that state-on-state conflict on the continent was a thing of the past.

Fox Walker, defence analyst at GlobalData, pointed to a number of ongoing European major land vehicle procurement efforts, often for high-end capability such as main battle tanks and infantry fighting vehicles, both types of platforms that combined account for the majority of land vehicle market spending.

“Hindsight is 20/20, but [former UK Prime Minister] Boris Johnson’s comment that we ‘have to recognise that the old concepts of fighting big tank battles on European land mass are over’ hasn’t aged well,” Walker said.

Examples include Poland’s procurement of 980 K2 MBTs – 800 of which will be produced in Poland – Lithuania’s acquisition of 120 Vilkas infantry fighting vehicles from Germany, and Hungary’s acquisition of 217 Lynx KF41 IFVs from Germany, point to the direction that European procurement is taking.

“These examples, among others, demonstrate the value that central and eastern European nations are placing on land vehicle procurement. These countries recognise the massive role that land vehicles have played throughout Russia’s illegal invasion of Ukraine and now seek to provide their armed forces with enhanced mobility and manoeuvrability,” Walker explained.

For Tristan Sauer, also a defence analyst at GlobalData, the Russian conflict in Ukraine highlighted the continued importance of vehicles in manoeuvre warfare, with the large numbers of platforms being acquired in European land programmes a “recognition” of the increased lethality of modern attritional warfare.

“This is something France has led the way in Europe since 2018/19 with the SCORPION modernisation programme, which saw the nation develop three new armored vehicles and a digitised vehicular C4ISR package in time and on budget with a focus on scalability, which was rather prescient in light of current trends,” Sauer explained.

Another major military power in Europe, the UK, is also embarked on a significant upgrade to its armoured land forces with the acquisition of the Ajax series of tracked armoured vehicles, as well as the ubiquitous Boxer personnel carrier.

Programmes such as the Common Armoured Vehicle System (CAVS) are also seeing significant traction in the continent, providing smaller militaries with capabilities that can actively augment and plug into wider Nato-scale battlegrounds. The CAVS platform developed jointly by Finland, Latvia and Estonia in 2020, with Germany and Sweden joining in 2023, and already has in excess of 450 vehicles on the order books.

Rare consensus within the European neighbourhood

The war in Ukraine – aside from the immense political, miliary, and humanitarian cost – is providing Western militaries with the opportunity to amend pre-2022 procurement plans in light of the changing face of the battlefield, and, in some cases, the apparent vulnerability of armoured vehicles to emerging threat from loitering munitions and improvised airborne suicide drones.

In some cases, as with France, the continent’s military operators appear to have been prescient in understanding that quantity has a quality all of its own, while others, such as the UK, have noted to efficacy and importance that long- and medium-range fires still have in combat.

Most European militaries are coming to the understanding the benefits of spiral development, meaning a platform enters service at 80-85% of desired capability, with upgrades following throughout the services life. This avoids the trap of waiting for a gold-plated capability only to final receive it many years too late, for a slight reduction in initial operating capability.

Despite comments from senior US politicians, it seems that Europe has taken onboard the need to better share the burden of Nato’s collective defence, driving spending into the land domain in a rare display of universal agreement amongst an often (diplomatically) fractious neighbourhood.